Inheritance tax is often misunderstood1 and causes fear in many more than the 5% of estates which currently pay it.

What might change? The Office of Tax Simplification and an All Party Parliamentary Group have made suggestions. Here are some possible changes, based on those and my own thoughts:

The rate: A reduction from 40% to 20% (if your IHT plan is to spend your money, that is the most fun way to do so – and you’ll probably suffer 20% VAT on most items. So a similar 20% tax on not spending has some logic.)

Exemptions and zero rates With a lowered rate, widening the base of those who pay may make sense, if the overall rate can be made acceptable. Removal of the capital gains tax free uplift on death where no IHT is payable – but deferral of the tax on those death gains until the asset is sold by the recipient.

Reliefs A cap on relief for business and farming assets, to perhaps £1m per person (currently unlimited) and the spreading of the tax payable over 10 or 20 years, to prevent the need to sell the business or farm just to pay the tax. Removal of relief for AIM shares.

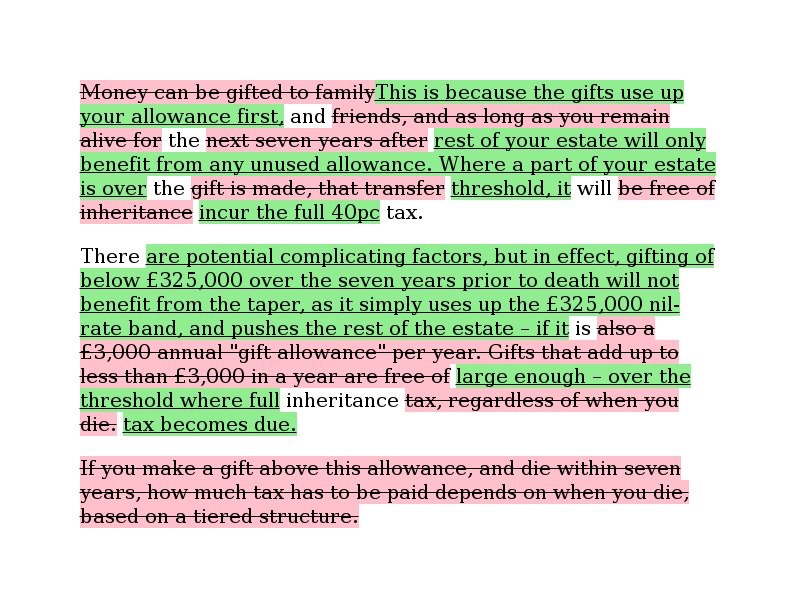

Gifts Reducing and simplifying the seven year gift period, removing minor multiple exemptions to one simple amount and reduced record keeping. A lower rate of tax (10%) on gifts.

Trusts Recognition that these can be part of a sensible plan to encourage gifts while protecting the gifted assets from being used unwisely by young beneficiaries. Simplification of the taxes on trusts.

What planning should take place now?

- Consider making gifts now

- Review assets qualifying for relief and consider trusts

- Review and update your will

- Consider life insurance level (often the easiest way to plan for IHT)

1 see https://blackshawtax.com/2019/11/12/inheritance-tax-houses-common-errors/